**Reasons Behind the Surge in Insurance Premiums**

**Ezra Croft’s Experience**

Ezra Croft, a homeowner from North Carolina, was taken aback when his annual homeowners’ insurance spiked to $1,600, marking a $700 increase. Despite never filing an insurance claim and residing in Raleigh, far from storm-prone areas, Croft found himself grappling with the unexpected rise in premiums.

**Financial Strain on Policyholders**

Expressing his astonishment, Croft, a middle-income individual, emphasized the financial strain caused by the sudden surge in his homeowner’s insurance costs. He voiced concerns about the affordability of maintaining his insurance coverage amidst the escalating premiums.

**Nationwide Trend**

Croft’s predicament is not an isolated case. Across the country, policyholders are facing similar challenges as insurance companies push for double-digit increases in homeowners’ premiums, with a notable 11% surge reported last year. The situation is even more dire in the auto insurance sector, where premiums are skyrocketing at a rate surpassing general inflation.

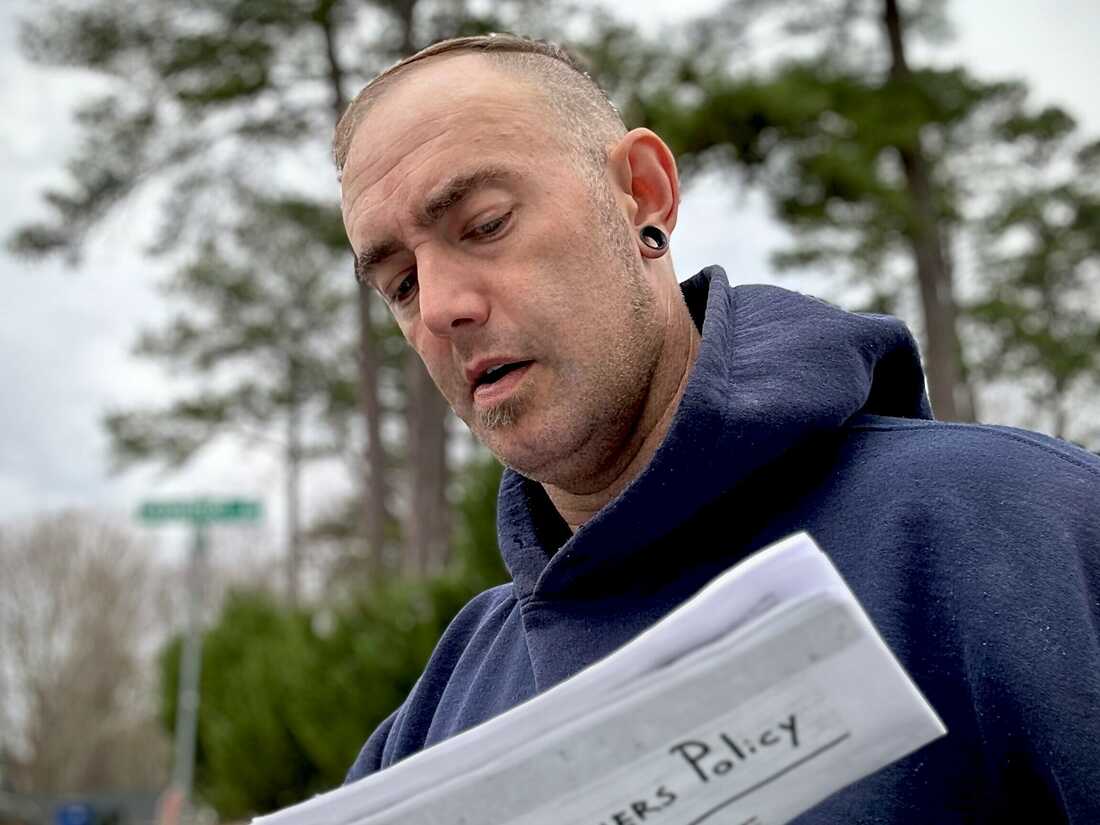

**Paul Morro’s Dilemma**

Illustrating this trend is Paul Morro, whose annual auto insurance bill surged by $600, despite both him and his wife working from home, thus eliminating any significant commuting factors. Morro, a resident of Herndon, Va., is bracing himself for the impending rise in his home insurance costs, echoing the sentiments of many who feel overwhelmed by the rapid escalation of expenses.

In conclusion, the surge in insurance premiums is a widespread issue affecting policyholders nationwide, driven by various factors that are contributing to the financial burden faced by individuals like Ezra Croft and Paul Morro.

Reasons Behind the Surge in Insurance Premiums

Insurance premiums are on the rise due to insurance companies striving to catch up after experiencing significant losses over the past two years. According to the Insurance Information Institute, for every dollar collected in home and auto premiums last year, insurers paid an average of $1.10 in claims and expenses.

Sean Kevelighan, the CEO of the institute, emphasizes the necessity for insurance companies to align their pricing with the prevailing risk levels. He acknowledges that while nobody welcomes higher bills, pricing must reflect the current risk landscape.

Inflation plays a significant role in driving up insurance payouts. The expenses associated with repairing or replacing damaged homes and vehicles have surged in recent years due to escalating labor and material costs.

Furthermore, insurers are grappling with a growing number of natural disasters across various regions, not limited to traditional disaster-prone areas like Florida and California.

Impact of Natural Disasters on Insurance Premiums

In the aftermath of a devastating landslide that destroyed a house and garage in the Hollywood Hills area of Los Angeles on Feb. 6, 2024, a car remains trapped in the wreckage. This event, caused by an atmospheric river storm, exemplifies the increasing frequency of natural disasters contributing to the surge in insurance premiums nationwide.

David McNew/AFP via Getty Images

Last year, the United States experienced approximately two dozen severe storms, each with billion-dollar price tags, unleashing lightning, hail, and destructive winds across various regions. Tim Zawacki, a principal research analyst for insurance at S&P Global Market Intelligence, notes, “While many of these storms may not make national headlines, their local impact is significant, leading to substantial costs. The industry is particularly concerned about the widespread occurrence of these events.”

Consequently, insurance premiums are on an upward trajectory, with no signs of slowing down this year, despite a general decrease in overall inflation. The reasons behind insurance premiums surging are directly linked to the escalating frequency and severity of natural disasters.

Dominance in Setting Insurance Premiums

Despite some regulatory control over insurance premiums surging reasons, insurers largely dictate pricing. Regulators are cautious as overly restricting premiums could lead insurers to withdraw coverage.

Doug Heller, the Consumer Federation of America’s insurance director, highlights insurers’ forceful tactics. Threats of market exit to secure demands have proven effective in influencing regulators.

In a Senate Banking Committee hearing on the property insurance market in Washington, D.C., Douglas Heller, the insurance director at the Consumer Federation of America, shared insights. The discussion took place on Sept. 7, 2023, with images credited to Anna Moneymaker/Getty Images.

The Treasury Department recently organized a roundtable involving consumer and environmental groups to address the impact of climate change on insurance markets. Further meetings with insurance industry stakeholders are also on the agenda.

Alicia Pitorri, a resident of Nashville, experienced a significant increase in her family’s auto insurance policy with Liberty Mutual, prompting a switch to State Farm for savings. Despite reducing costs, Pitorri still faces higher expenses compared to two years ago.

Acknowledging the necessity of insurance for vehicles and homes, Pitorri emphasizes the importance of managing expenses amidst surging insurance premiums. She highlights the need to prioritize insurance payments while making adjustments in other areas to maintain essential coverage.